Share:

We work with HR professionals in a variety of businesses—some who are new to the benefits industry and others who have spent decades in the field. Total rewards is a relatively recent invention from the aughts, but the roots of what most employees expect today go back nearly 400 years!

And from the start, it was all about recruitment and retention:

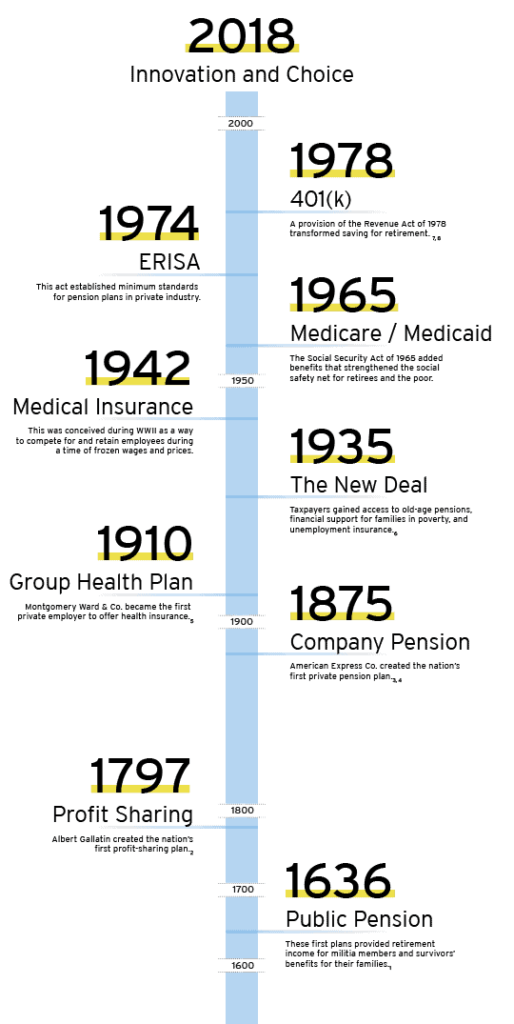

1636: The first public pensions emerge

Before American independence, there was a need for law and order. And that meant recruiting citizens to staff armed militias in Plymouth, and eventually the rest of the colonies, long before the war. These first plans provided retirement income for militia members and survivors’ benefits for their families.

1797: Private industry starts sharing the wealth…

As this growing nation was in need of skilled and trainable workers, industrial employers needed a way to retain their craftsmen. Albert Gallatin created the nation’s first profit-sharing plan at his glassworks not far from Pittsburgh, giving employees a stake in the company’s profitability and allowing them to be incentivized in a way that hadn’t before.

1875: …and finally embraces pensions

American Express Co. began as a freight and valuables delivery service at a time when the U.S. Postal Service was viewed as less than reliable. It would also become the first private employer to follow the government’s example and create the nation’s first private pension plan, providing security for the elderly and disabled.

1910: The first group health plan

Chicago was the mecca of the early mail-order industry, and competitors Sears, Roebuck and Company and Montgomery Ward & Co. were neck-and-neck for business and workers. Ward became the first private employer to offer health insurance to its workers, but such benefits wouldn’t become commonplace until the 1940s.

1935: The New Deal

The sweeping nationwide changes brought about by the Social Security Act of 1935 would mandate a basic level of financial stability in old age. Immediately, taxpayers had access to old-age pensions, financial support for families in poverty, and unemployment insurance. By 1956, the system would add income protection for disabled workers and their dependents.

1942: WWII triggers a benefits revolution…

As people went off to war, severe labor and raw material shortages required federal legislation that froze wages, salaries, and prices. While such laws stabilized the wartime economy, it left private employers with a conundrum: how to keep workers when they couldn’t raise pay. This would lead to the first major medical insurance plan , which was offered to General Electric executives as a way to compete for and retain employees.

1965: …as did the War on Poverty

The Social Security Act of 1965 would create the Medicare and Medicaid programs that added guaranteed healthcare benefits for retirees, as well as for workers in low-paying jobs that didn’t receive such benefits. And like the World War II aftermath, the rising tax environment called for further expansion of corporate incentives to retain employees that would support richer and more widespread private health, disability, and retirement plans.

1974: ERISA

The Employee Retirement Income Security Act of 1974 (ERISA) established minimum standards for pension plans in private industry, leading to a whole new level of financial and management disclosure and court remedies. ERISA would revolutionize both the benefits field and the human resources function that we know today.

1978: Section 401(k)

The Revenue Act of 1978 included a provision called Section 401(k). As we now know, that provision gave employees a tax-free way to defer compensation from bonuses or stock options, effective January 1, 1980. That small provision became a movement that not only changed how employees saved for retirement, but shifted certain benefits decisions from the nation’s employers to the nation’s workers—an enormous cultural shift for the workplace.

Today: Innovation and choice

The Society for Human Resource Management’s 2017 Employee Benefits Report shows that 68% of organizations revealed during 2016 that they were experiencing recruiting difficulties and skills shortages for important job categories. With such steep competitive challenges facing so many organizations, no wonder we’re seeing increased individualization in the benefits process. It’s no longer about checking boxes for large groups—it’s about connecting each person with benefits they really care about through a total-rewards mindset.

The total-rewards movement is also creating significantly more important roles in HR and benefits. These professionals are helping their organizations master this learning curve in the evolving expectations of employees.

Attracting the best workers 40 years ago meant creating competitive, company-directed group packages in two categories: health and retirement. Today, those elements remain the top priority at most companies—along with PTO, performance bonuses, and paid sick days—but customization is key.

And so are work/life and convenience benefits. The report also shared that over the past five years, an almost 60% increase occurred in telecommuting on an ad-hoc basis, with casual dress codes and flextime programs on the rise. And for younger workers, travel perks such as points retention and airline / rental-car class upgrades pair nicely with more adjustable work schedules.

Looking ahead

So what have we learned from this rich history? Certainly that it’s important to know the major milestones of our industry so we can understand its evolution. But to create the best workplaces today, it’s essential to listen to workforce needs and goals at the individual level.

In fact, in 2018, the organization with this conception of benefits will continue to attract the best workforces, foster the greatest employee loyalty, and create the most value for their company.

Talk about making history.

Citations: